Real Estate Investing

Make Money Using Real Estate as an Investment Vehicle

It can be tricky and time consuming to turn a goose egg into a nest egg, but if you're fortunate enough to have good credit, good sense, and a bit of money, whether its $20,000, or $200,000, that capital can be multiplied dramatically using real estate investments as the vehicle. The intention of this article is first, to detail a traditional process for the accumulation of wealth and second, to demonstrate just how $200,000 in cash can become $2,000,000 within a reasonable period of time (determined by you based upon your aggressiveness, creativity, insight, understanding, goals, etc.) without taking extraordinary risks.

Real Estate Investing Advice - How to make $2,000,000 from only $200,000

Let's assume you have $200,000 in investment capital, and you want to accumulate equities of $2,000,000 so that you will be able to retire with an income of $100,000 per year even if your equities only produce a conservative annual cash flow return of 5%. To keep your purchases within real world parameters, each acquisition and disposition will be made with the following conditions:

- The Down Payment is 25% of the purchase price

- The Transaction Fees are 2% of the purchase price and include such things as loan fees, property tax and insurance pro-rations, title fees, etc.

- The Costs of Disposition are figured at 7% of the Exchange Value and are made up of a 6% commission and miscellaneous fees and pro-rations

- Each property will be held until it can be sold for 40% more than its original acquisition price

In the following three stages, from the inception of your investment to reaching your objective, when you move from one property to the next, it will be utilizing tax-deferred exchanges. This will allow you to move from your initial investment to the final transaction without the burden of paying capital gains taxes along the way. This is not a tax-free transaction, but merely a tax deferral. Nonetheless, it is a common and effective method of capital preservation and estate building. Each time you exchange one of your investments, the property you are disposing of (In IRS technical terms this is the “relinquished” property, and in investment/exchanger jargon is the “down-leg” property.) will be charged 7% of the exchange value (this would be the sales price if you were selling instead of exchanging) for Disposition Costs.

Before we start looking at the examples, I should note that in actual practice you would consider all of the factors through which you make money from your investment; primarily cash flow, principal debt reduction, and tax benefits, in addition to the investment's increase in value. However, for our purposes here we'll consider that all of the income generated in the “building period” will be used entirely for expenses and improvements to the asset in order to maximize the property values more rapidly. The whole point of this discussion is to introduce you to “forced appreciation” – the ever-present opportunity for you to manufacture wealth.

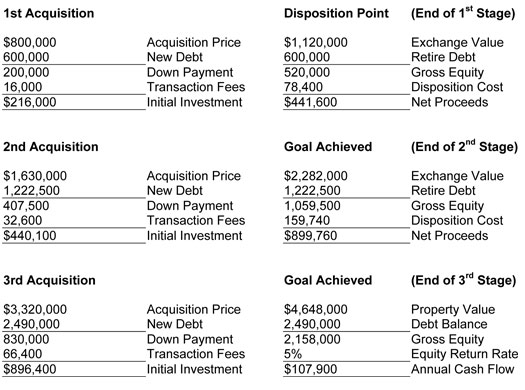

Now for the numbers: Your first purchase is an $800,000 multi-family building. You make a reasonable 25% down payment ($200,000) and pay transaction fees of $16,000. When its value increases to $1,120,000, 40% above its acquisition value, you relinquish your 1st stage property. As a result of this disposition, you would retire the debt, $600,000, and pay your transaction fees of $78,400 (7%) leaving you with net proceeds of approximately $441,600 for use in acquiring the 2nd property. The second acquisition and the third, follow in like manner. Please note that in the following, the New Debt and the Retired Debt or bordering-on-over-simplified-example, Debt Balance is identical. This could only take place in the unlikely event that during the holding period you secured an interest only loan and no principal payments were made. This was necessitated here because the time period for amortization is unknown and therefore the amount of debt reduction uncertain. However, there is no need to quibble over interest rates, loan terms, etc. Too many details can blur the main point: you can manufacture wealth on your schedule using your creativity, your ability, your time, your effort and your good common sense. Below is the simplified process of just how this would unfold.

Simple. Straight forward. Nothing tricky. You just moved a $200,000 investment into gross equity of $2,158,000, which produces an annual income in excess of $100,000 per year!

Now, let's bring time into the equation. After all, if it took you 30 years to increase your original $216,000 investment capital to $2,158,000 in gross equity, 10 years per turn, that would be an increase of 8%± per year, compounded annually. Not bad. Better than the long term average of the stock market? You bet - even without considering cash flows, debt reduction, or tax savings! Of course, when you figure inflation at even a moderate rate of, say 3% annually, your real gain, while reasonable, is quite a bit lower. On the other hand, if you were able to accomplish this same feat in 10 years, your return would be over 25% per year, or in 6 years 46%.

So the obvious question is, “How long does this take?” Here's the stunner. In the past few years, in both good markets and bad, we have seen instances of investment properties increasing 30%+ in value within six months. Of course, when a property increases 30% per year and the initial investment was 25% of the purchase price or less, the result is an increase on your investment of over 100% per annum!

But let's not dwell upon the unusual, let's just consider what a reasonable investor can accomplish within a reasonable period of time, under reasonable circumstances. In the first example, we considered an investor who purchased an $800,000 building with investment capital of $200,000. This is 3:1 (three-to-one) leverage. The investor is leveraging his $200,000 with $600,000 of borrowed capital, thereby purchasing an $800,000 property. In each case, the investment is held until it increases its value 40%. This increase in value may occur in an infinite number of ways. However, the value of an income producing investment increases basically for four reasons:

- The income increases

- The expenses decrease

- There is a change in investors' perceptions that make an income producing real estate investment more desirable to own, i.e. other investment vehicles have proved to have unwarranted risk or to be otherwise less desirable

- The general perception of investors shifts so that they are willing to accept a lower return on their investment capital

As an aside, it is interesting to note that perceived risk is a most important factor in an investor's decision as to where to place capital. As investors discern that a segment of the market, or a geographical location, or a particular investment vehicle contains less risk or offers greater rewards than the available alternatives, historical returns will decrease simply by the clamoring of investors for that desirable destination and the corresponding lowering of return expectations. It's pure supply and demand.

Let's just focus upon increasing the Gross Income, as this is the key factor that will affect most investors – those who buy income producing investments of two to eight multi-family units. This is true because, in this most popular segment, most investors rely on the Gross Rent Multiplier (GRM) in making their preliminary investment decisions. This is because detailed financial information is commonly neither readily available nor dependable. The GRM is simply the property value or asking price divided by the Annual Gross Income.

The exciting part of all this is that an owner is totally in control of rents. This puts the owner squarely in control of his investment destiny rather than being the victim of external forces. It's important to recognize this point – most owners don't. This is the key to shortening the holding periods necessary to achieve rapidly increasing equities. You do not need to sit and wait for your property to appreciate over time. You can force the value of your investment to increase … often dramatically. You are in control and in that position you can manufacture, at a reasonable level, the value of your investments.

This is not new thinking. This is not original. This is not creative. This is old fashioned, hard-nosed, tried and true, simple, basic, primary, not-to-be-denied, bedrock investment principle. Let us share a quick story to illustrate this critical point.

We have recently seen an investor pay $535,000, with a 14 GRM, for a triplex rental property. Just over a year after the initial purchase the investor sold the building for $695,000 with about a 13 GRM, which produced a return of over 60%.

The triplex was in pretty good shape but it did need some minor structural work that cost about $5,000. Initially, it rented for $38,200 per year. Each of the three units had 2 bedrooms, but one of the units was quite large –large enough so that two additional bedrooms could be added by moving a few walls. Cost? $10,000. The investor put 20% down and incurred closing costs of about $3,000. Total investment was about $125,000 ($107,000 down payment + $3,000 closing costs + $15,000 repairs). When the sale was closed, the net proceeds were about $224,000 ($695,000 selling price minus $428,000 mortgage minus $43,000 costs of sale). What was the profit? $224,000 net proceeds from the sale minus the $140,000 initial investment equaled $84,000, plus $1,500 in cash flow during the holding period or $85,500. ($85,500 / $140,000 = 61% return on investment)

The significance of this example is not to be found in the strong return, which was made, incidentally, in a stagnant market with most investors sitting on the sidelines in abject indecision, spending their time being concerned with the direction of the overall market rather than searching for money making opportunities. The point is that value can be manufactured. In this case the investor increased the property's income from $38,200 to $53,500 (40%±) by adding bedrooms and slightly increasing the rent per bedroom. The rent per bedroom only increased from an average of 5% ($530 to $557), but now there were eight bedrooms to rent rather than six!

This is a classic case of driving value upward and clearly illustrates this dynamic principle. The value of income producing properties is derived in direct proportion to the income it produces. Increasing a property's income is the secret to rapid increases in value and has been the key factor in the accumulation of wealth for many investors. It could well be the key to amassing your fortune and successfully achieving your estate planning goals.